What You Need To Understand About Mortgages For Your Home

Created by-Crowley SpiveyFinding a home mortgage that is works for you can sometimes be a tricky endeavor. If you are interested in learning about different types of mortgages and reading various tips to help in this area, then you will want to read the following article. Keep reading to help you gain the knowledge necessary so you aren't lost when searching for a home mortgage.

Your job history must be extensive to qualify for a mortgage. In many cases, it's the norm for a home lender to expect buyers to have been in their job position for two or more years. Changing jobs often could make you ineligible for mortgages. Don't quit in the middle of an application either! It makes you look unreliable.

Gather all needed documents for your mortgage application before you begin the process. These documents are the ones most lenders require when you apply for a mortgage. Income tax returns, W2s, bank statements and pay stubs are usually required. If you have the documents in hand, you won't have to return later with them.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If you don't have your paperwork in order, your mortgage may be delayed.

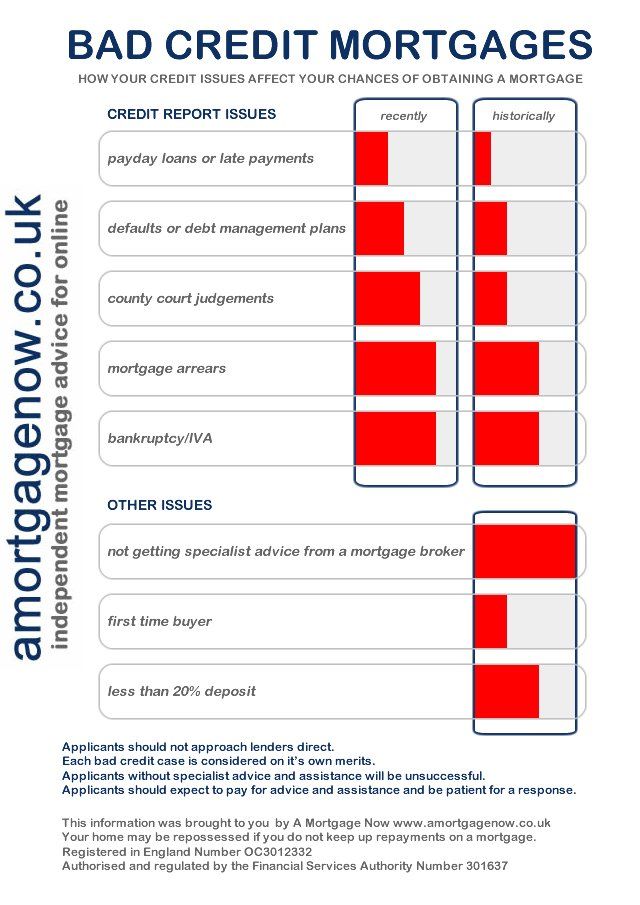

Try shopping around for a home mortgage. When you do shop around, you need to do more than just compare interest rates. While they're important, you need to consider closing costs, points and the different types of loans. Try getting estimates from a few banks and mortgage brokers before deciding the best combination for your situation.

Don't forget to calculate closing costs when applying for a mortgage, particularly if this is your first time. Above and beyond the down payment, numerous charges exist simply for processing the loan, and many are caught off guard by this. You should anticipate paying up to four percent of the mortgage value in total closing costs.

After https://www.bloomberg.com/news/articles/2021-11-23/advent-centerbridge-offer-to-buy-german-real-estate-bank-aareal 've been approved for your home mortgage and are ready to move in, consider starting a home emergency fund right away. Being a homeowner means always being prepared for the unexpected, so having a stash of cash stored away is a very smart move. You don't want to have to choose between paying your mortgage and fixing a hole in the roof down the road.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. Each lender is different, so ask in advance and be well prepared.

Pay down your debt. You should minimize all other debts when you are pursuing financing on a home. Keep your credit in check, and pay off any credit cards you carry. This will help you to obtain financing more easily. The less debt you have, the more you will have to pay toward your mortgage.

If you are having difficulty paying a mortgage, seek out help. Look into counseling if you are having trouble keeping up with your payments. There are government programs in the US designed to help troubled borrowers through HUD. These counselors offer free advice to help you prevent a foreclosure. Call or visit HUD's website for a location near you.

ARM, or adjustable rate mortgages, don't expire near the term's end. The rate is sometimes adjusted, however. It can good for some people, but it puts a borrower at risk for high interest rates.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

After getting a home loan, try paying a little extra on the principal each month. This will help you pay off your loan much faster. For instance, if you pay a hundred dollars more toward your principal, you can reduce your loan term by ten years or more.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. simply click the following article could open a new avenue of financing up for your new home mortgage.

Always read the fine print. If you have a hard time understanding the information, get some help with an expert that does not work for the lending company. You want to make sure that the terms do not change after a certain amount of time. The last thing you want is surprises.

Boost your chances at of a lower mortgage rate by visiting your lender several months before submitting an application. Time is vital in the mortgage process.

Meeting with the lender months beforehand can help you fix issues like credit scores that could raise your rates. Usually when your offer is accepted, you will be quickly heading towards your closing date. This leaves little time to fix anything that could lower your rate.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

There are a lot of fees associated with the process of purchasing a home and you should have them put to the side prior to applying. If a lender sees that you have enough money set aside to pay for all of your closing costs, they may be more likely to approve your loan.

Your home is likely your home because of the mortgage that you have taken out. With this new information, you have new ways to improve your own situation. Enjoy your home for many years by following the great advice above to get the mortgage that is right for you.